At its core, accounts receivable accounting is simply the way you track and collect the money your customers owe you for goods or services you’ve already delivered. This isn't just another line item; it's a crucial asset on your balance sheet that shows your company's real-world ability to turn sales into cash. According to financial experts, managing this asset effectively is a cornerstone of corporate financial health (Investopedia, 2023).

Why Accounts Receivable Is Your SME’s Lifeline

Picture your business as a local shop. A regular customer picks up some groceries and says, "Put it on my tab, I'll pay you at the end of the month." That tab? That's your accounts receivable (AR). Now, scale that up. Imagine dozens of customers, each with their own tab, all due at different times. Accounts receivable accounting is the system you use to keep all those tabs organised, making sure every promise to pay turns into actual money in your bank.

For small and medium businesses across Africa, this isn't just about tidy bookkeeping—it's the lifeblood of the company. If you don't have a steady stream of cash coming in from customers, how can you pay your suppliers, cover payroll, or invest in growing your business? It becomes nearly impossible. Think of effective AR management as the engine that keeps your entire operation running. As a study by Atradius highlights, managing trade credit and receivables is critical for SME survival, especially in emerging markets (Atradius Payment Practices Barometer, 2022).

The Real-World Challenge for African Businesses

Sadly, keeping this lifeline flowing is a massive headache for entrepreneurs in markets like Nigeria, Kenya, and South Africa. Chronic late payments are a huge problem. So is the sheer chaos of trying to track everything manually in spreadsheets or notebooks, which just creates bottlenecks. An invoice you’ve sent out isn’t the same as cash in hand, and that gap can put a serious strain on even the most promising businesses.

This isn't just an isolated issue; it's a systemic one. Take South Africa, where accounts receivable challenges are particularly stark. Businesses there often wait an average of 45-60 days for payments. This delay hits 55% of small enterprises hard and drives up their operational costs by 20-30% simply from the manual effort of chasing down what they're owed. You can find more insights on these economic pressures from the African Development Bank Group.

An organised accounts receivable process transforms a list of unpaid invoices from a source of anxiety into a strategic tool. It provides the data needed to forecast cash flow, identify your most reliable clients, and spot potential payment issues before they escalate. This is supported by principles outlined by the Corporate Finance Institute (CFI, 2022).

From Bookkeeping Chore to Strategic Advantage

It’s easy to look at accounts receivable as just another tedious chore, but that’s a massive missed opportunity. When you manage it properly, you strengthen your business from the inside out. It makes your interactions with clients more professional, building trust through clear, accurate, and timely invoices and statements.

Ultimately, mastering your AR process does more than just make sure you get paid. It gives you the financial stability and predictability you need to make confident business decisions. This is how you build a resilient company that doesn't just survive but actually thrives in a competitive market, turning promises of payment into the fuel for real, sustainable growth.

The Story of an Invoice in Your Books

Accounts receivable accounting can feel a bit abstract, full of debits and credits that don’t always seem connected to the real world. So, let’s bring it down to earth.

Imagine you run a bustling marketing agency in Nairobi. You’ve just wrapped up a major campaign for a client, and it's time to get paid. This is the story of that invoice, told through the language of your accounting books.

Each step in this journey creates a journal entry, which is just a formal record of a financial transaction. Think of it like a diary entry for your business's money, making sure everything adds up and stays balanced.

Of course, it's not always a simple story. The real world throws curveballs that can turn a straightforward process into a major headache.

As you can see, a simple late payment can quickly spiral into manual chaos, putting a serious squeeze on your company's cash flow.

Step 1: Issuing the Invoice and Recognising Revenue

The moment you send your client an invoice for KSh 100,000, you’ve officially earned that money—even if the cash isn't in your bank account yet. In accounting terms, this is called revenue recognition. You need to record this right away to keep your financial statements accurate, following principles like ASC 606 or IFRS 15.

Your first journal entry will look like this:

- Debit Accounts Receivable KSh 100,000: You're increasing your Accounts Receivable (an asset), because someone now owes you money.

- Credit Revenue KSh 100,000: You're increasing your Revenue account, showing your business has made a sale.

This simple entry tells a crucial part of your business's story: you're growing and generating sales. For some pointers on crafting invoices that get noticed and paid, check out our detailed examples of invoices.

Step 2: Recording the Payment

A few weeks later, your client pays the full amount via M-PESA. Great news! Now, you need to update your books to show the cash has arrived and the client's debt is cleared. This is a step where many businesses slip up, leaving paid invoices as "outstanding" and skewing their whole financial picture.

The second journal entry is just as straightforward:

- Debit Cash KSh 100,000: Your Cash account increases because money has come into the business.

- Credit Accounts Receivable KSh 100,000: Your Accounts Receivable asset decreases because the client no longer owes you this specific amount.

See how the Accounts Receivable account for this invoice is now balanced back to zero? The story is complete. The promise of payment has turned into actual cash.

A core principle in accounting is that every debit must have an equal and opposite credit. This "double-entry" system is the secret to keeping your books perfectly balanced at all times. When you debit AR, you have to credit another account (like Revenue) to keep the financial equation in check. This principle dates back to Luca Pacioli in the 15th century (Sangster, 2016).

Step 3: Handling Adjustments Like Discounts

But what if you offered the client a 2% discount for paying within 10 days? If they take you up on it, they’d pay KSh 98,000, not the full amount. You'd need one more entry to close the loop properly. This final step records the cash you received and also accounts for the KSh 2,000 discount you gave away.

Here’s how you'd record it:

- Debit Cash KSh 98,000: To show the actual cash that hit your account.

- Debit Sales Discounts KSh 2,000: This is an expense account that tracks the cost of the discounts you've offered.

- Credit Accounts Receivable KSh 100,000: To completely clear the full, original invoice amount from your books.

This ensures your records accurately reflect not just the payment, but also the cost of that early payment incentive.

Manual vs Automated AR Journal Entries

Following this story for a single invoice is simple enough. But now, imagine you're juggling dozens, or even hundreds, of them every month. Manually tracking all this in spreadsheets quickly becomes a recipe for mistakes, missed payments, and hours of wasted time.

This is exactly where automation changes the game. Let's compare the old way with the new way.

Comparison Table: Manual vs Automated AR Journal Entries

Here’s a quick look at how tedious a manual process is compared to a platform like CRM Africa, even for just one invoice.

| Accounting Step | Manual Process (Using Spreadsheets) | Automated Process (Using CRM Africa) |

|---|---|---|

| Invoice Creation | Manually type up the invoice, save it as a PDF, find the right email, and attach it. | Generate a professional, branded invoice from a template and email it directly from the platform in a few clicks. |

| Revenue Recognition | Open your accounting software or spreadsheet and manually create the Debit AR / Credit Revenue journal entry. | The journal entry is automatically created and posted the moment the invoice is sent. Zero manual work required. |

| Payment Recording | Get a payment notification, hunt for the right invoice in your spreadsheet, then manually create the Debit Cash / Credit AR entry. | The client pays via an integrated gateway (like M-PESA or Paystack). The system automatically records the payment, matches it to the invoice, and creates the journal entry. |

| Error Checking | Spend hours at the end of the month painstakingly comparing bank statements to spreadsheets to find typos and missed entries. | Reconciliation happens in real-time, automatically. The system flags any discrepancies instantly, so human error is virtually eliminated. |

The difference is night and day. Automation doesn't just save you time; it gives you a clearer, more accurate view of your finances, letting you focus on running your business instead of chasing paperwork. Studies by groups like Gartner have shown that automation can reduce manual accounting tasks by over 80% (Gartner, 2021).

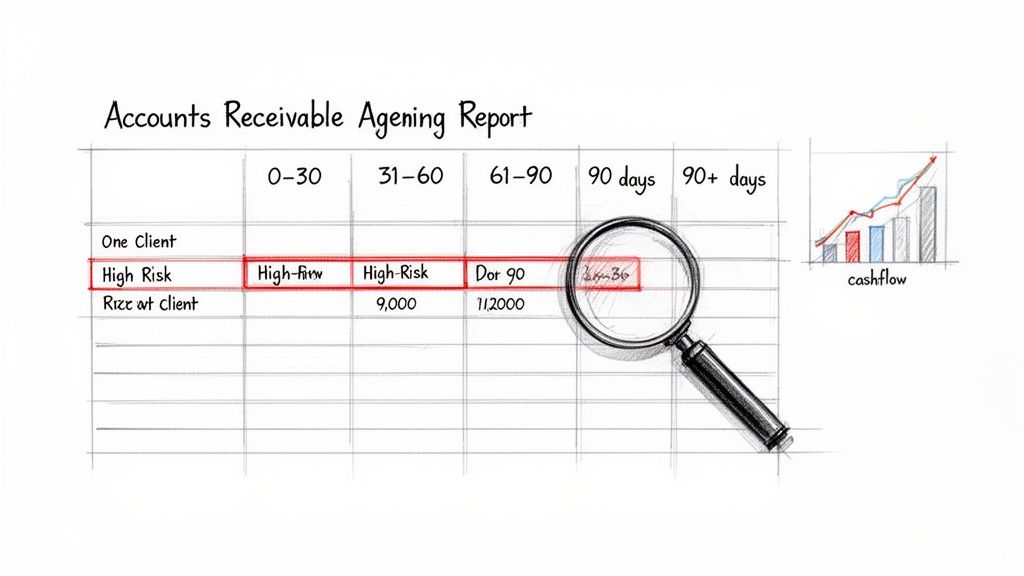

Using an Ageing Report to Predict Your Cash Flow

If you had to pick just one tool to keep a finger on the pulse of your business’s financial health, what would it be? For me, the answer is easy: the accounts receivable ageing report. Don’t let the name fool you; this isn’t some complex financial statement. It’s a simple schedule that acts as a powerful early warning system for your cash flow.

Think of it as a quick health check for all the money you’re expecting. The report neatly sorts all your unpaid invoices into buckets based on how long they’ve been outstanding — usually 0-30 days, 31-60 days, 61-90 days, and 90+ days. This simple breakdown instantly shows you who's paying on time and, more importantly, whose overdue balance is starting to become a risk.

This report helps you see past the total amount you’re owed and understand the quality of that debt. An invoice that’s 10 days old is a healthy, reliable asset. One that's creeping past 100 days? That's a massive red flag. The truth is, the longer an invoice goes unpaid, the less likely you are to ever see that cash. Data from commercial credit agencies consistently shows that the probability of collecting a receivable drops significantly after 90 days (Coface, 2023).

Reading the Report for Actionable Intelligence

An ageing report isn’t just for looking at; it’s a tool for action. It transforms a messy list of outstanding invoices into a clear roadmap for your collection efforts. For any business owner, whether in Ghana or Egypt, this means you can start making proactive financial decisions instead of constantly reacting to cash shortages.

A quick scan of the columns tells you exactly where to focus:

- Spot High-Risk Clients: See a client with a big balance consistently stuck in the 60+ day column? They need your immediate attention. Are they having financial problems, or is there a disputed invoice you need to sort out?

- Prioritise Collection Calls: Stop calling clients at random and start focusing your energy where it matters most. Tackle the largest, oldest debts first to make the biggest impact on your cash flow.

- Improve Cash Flow Forecasts: The report gives you a realistic picture of when money will likely arrive. If a huge chunk of your receivables is over 60 days old, you can't budget as if that cash is coming in next week.

An accounts receivable ageing report helps you estimate a realistic value of your receivable assets. Generally accepted accounting principles require businesses to plan for uncollectibility, and this report is the primary tool for making that estimate accurately (Kieso, Weygandt, & Warfield, "Intermediate Accounting").

An Example of a Basic Ageing Schedule

Let’s say you have three clients. A quick glance at a simple ageing schedule immediately tells a story about each one, helping you decide what to do next.

| Client Name | Total Owed | Current (0-30 Days) | 31-60 Days | 61-90 Days | 90+ Days |

|---|---|---|---|---|---|

| Client A | R15,000 | R15,000 | R0 | R0 | R0 |

| Client B | R25,000 | R5,000 | R20,000 | R0 | R0 |

| Client C | R12,000 | R0 | R0 | R2,000 | R10,000 |

Right away, you can see Client A is in good standing. Client B is a little behind and needs a friendly reminder for the invoice in the 31-60 day bucket. But Client C is the immediate priority. With the bulk of their debt now over 90 days past due, the risk of it becoming a bad debt has shot up. This is a much clearer picture than just knowing you are owed a total of R52,000. To see how these reports feed into your wider client communications, check out our guide on creating a professional statement of account.

Automation Turns Data into a Dashboard

Let's be honest, manually creating and updating an ageing report in a spreadsheet is a tedious job, not to mention it’s ripe for human error. This is exactly where modern software like CRM Africa changes the game.

Instead of painstaking data entry, the system automatically generates a real-time ageing report for you. Every time an invoice is sent or a payment is logged, the report updates instantly. It transforms a static, outdated spreadsheet into a living, breathing dashboard for your accounts receivable accounting. This empowers you to make smart, forward-thinking decisions that keep your cash flow healthy and predictable.

Navigating Bad Debts and Invoice Write-Offs

No matter how solid your client relationships are, you’ll eventually run into an invoice that just won't get paid. It's an unfortunate, but very real, part of doing business. When a customer can't or won't settle their bill, you need a clear game plan. This isn't just about tidying up your books—it's about making sure your financial records tell the true story of your company's health.

Getting this right is a core part of accounts receivable accounting. If you let uncollectible invoices linger, you'll end up with distorted financial reports. Your assets will look bigger than they actually are, giving you a false sense of security about your cash flow.

Direct Write-Off vs. The Allowance Method

When it’s time to accept that an invoice is a lost cause, you have two main ways to account for it. Picking the right one for your SME comes down to understanding the difference.

-

The Direct Write-Off Method: This is the most straightforward route. You simply wait until you’re positive an invoice is uncollectible, then you write it off directly as a bad debt expense. It’s easy, sure, but it’s not always the most accurate because it records the expense long after the original sale happened and is not compliant with GAAP for most public companies.

-

The Allowance Method: This one is more proactive and is the gold standard for accurate financial reporting. Instead of waiting for specific invoices to go bad, you look at the bigger picture. You estimate a percentage of your total receivables that you expect won't be collected and set aside an "allowance" for them from the get-go.

Think of it this way: Generally accepted accounting principles require businesses to show a realistic value for their assets. The allowance method helps you do just that. It creates a "contra-asset" account that offsets your total accounts receivable, giving you a much clearer picture of the cash you can realistically expect to see in the bank. This aligns with the matching principle in accrual accounting (AccountingTools, 2023).

Which Method Is Right for Your SME?

For most SMEs, especially those in the early stages, the direct write-off method is often perfectly fine. It’s simple and gets the job done.

But as your business grows and you’re managing a higher volume of invoices, switching to the allowance method will give you a far more accurate financial snapshot. That kind of clarity is crucial when you're trying to forecast cash flow or secure financing.

Sometimes, unpaid invoices create a serious cash crunch. When this happens, some businesses look for external solutions. The Africa accounts receivable financing market, valued at USD 164.06 billion, is expected to climb to USD 250.28 billion by 2029. This isn't surprising, as businesses across nations like South Africa are looking for ways to bridge the cash gaps left by slow-paying clients. You can dive deeper into these market dynamics and forecasts on Research and Markets.

How to Write Off a Bad Debt

Let's walk through an example. Imagine you've tried everything to collect on a R5,000 invoice, but it’s clear the money isn't coming. Here’s how you’d record the loss using both methods.

Using the Direct Write-Off Method

Your journal entry is simple. You’re just recognising the loss.

- Debit Bad Debt Expense R5,000: This increases your expenses for the period.

- Credit Accounts Receivable R5,000: This removes the uncollectible amount from your assets.

Using the Allowance Method

Here, the process is a bit different. You don't hit your expense account at the time of the write-off because you already accounted for it when you made your estimate. Instead, you use the allowance you created.

- Debit Allowance for Doubtful Accounts R5,000: This draws down the "cushion" you set aside.

- Credit Accounts Receivable R5,000: This removes the specific bad invoice from your books.

This two-step process—estimating first, writing off later—smooths out your expenses over time. It prevents one large bad debt from skewing a single month's profitability, giving you and any potential investors a more stable and realistic view of your business performance.

Actionable Steps to Streamline Your AR Process

Let’s be honest, turning your accounts receivable from a manual, slow-moving headache into a well-oiled cash flow engine isn’t just a nice idea—it’s essential for survival and growth. You can get control of your cash flow by putting a few solid best practices in place. These steps will shorten payment cycles, cut down on friction, and make your brand look more professional. This is your roadmap to getting paid faster and more reliably.

The very first move? Get rid of any grey areas in your agreements. Vague terms are basically an open invitation for late payments. When you establish crystal-clear policies right from the start, you set a professional tone and manage your client’s expectations from day one.

Establish Unambiguous Payment Terms

Your invoices and contracts should leave absolutely no room for guesswork. Clearly state your payment deadlines, the payment methods you accept, and any penalties for late payments or discounts for early ones. This simple act of clarity is the foundation of a healthy accounts receivable accounting system.

For example, terms like “Net 30” (meaning payment is due in 30 days) are pretty standard. But why not add an incentive like “2/10 Net 30”? This offers a 2% discount if the bill is paid within 10 days. You'd be surprised how powerful that small discount can be in getting clients to prioritise your invoice. You can learn more about creating effective invoices in our guide on free invoicing software for small businesses.

A proactive approach to collections will always beat a reactive one. By setting clear expectations upfront, you prevent most payment disputes before they even start, which saves you time and keeps client relationships strong. A study in the Harvard Business Review supports this, noting that clarity in communication is key to efficient business operations (HBR, 2019).

The move towards automation is a massive deal right now. In South Africa, for instance, the accounts receivable automation market hit a value of USD 114.5 million and is expected to rocket to USD 292.5 million by 2030. This kind of rapid growth shows just how crucial it is for businesses to modernise how they invoice and collect payments if they want to stay in the game. You can dig into these insights on Grand View Research.

Offer Diverse and Convenient Payment Methods

In a market as diverse as Africa, making it dead simple for clients to pay you is non-negotiable. The more friction you can remove from the payment process, the faster the cash will hit your account. Sticking to only traditional bank transfers is a surefire way to slow things down.

Instead, you need to embrace the payment methods your clients are actually using every day. That means integrating the solutions that are popular all across the continent.

- Mobile Money: Platforms like M-PESA, MTN Mobile Money, and Airtel Money are absolute must-haves in many regions.

- Online Gateways: Services like Paystack, Flutterwave, and Pesapal make card and bank payments a breeze.

- Direct Debit: For recurring services, setting up automated debits ensures you get timely, predictable revenue streams without any hassle.

By offering a bunch of convenient options right on your invoice or through a client portal, you’re empowering clients to settle their bills with a single click.

Leverage Automation for Reminders and Follow-Ups

Manually chasing overdue invoices is one of the most soul-destroying and time-consuming tasks for any business owner. It kills your productivity and can easily put a strain on good client relationships. This is exactly where automation becomes your best friend.

Modern platforms can automate the entire follow-up sequence for you. Imagine setting up a workflow of polite, professional reminders that go out automatically as an invoice gets close to its due date, on the day it’s due, and at set intervals after it becomes overdue. This consistent, gentle prodding keeps your invoice top-of-mind without you having to lift a finger.

This frees up your team to focus on work that actually grows the business. To really take your AR process to the next level, you might even consider specialised support and hire an Accounts Receivable Virtual Assistant who can manage everything from invoicing to collections.

Ultimately, combining clear policies, flexible payment options, and smart automation creates a truly robust system. It transforms your accounts receivable process from a constant source of stress into a reliable driver of business growth, ensuring healthy cash flow and stronger client partnerships.

Got Questions About Accounts Receivable? We've Got Answers.

Jumping into the world of accounts receivable can feel like trying to learn a new language. You’re busy delivering amazing products and services, but those nagging questions about debits, credits, and cash flow are always there. To help clear things up, we've pulled together some of the most common questions we hear from entrepreneurs across Africa.

These aren't textbook theories; they're the real, practical queries that pop up when you're in the thick of running your business. Getting straight answers is the key to managing your money with confidence and making your accounts receivable work for you.

What's the Difference Between Accounts Receivable and Accounts Payable?

This is one of the first hurdles for any new business owner, but the answer is refreshingly simple. Just think of it as a two-way street for your money.

Accounts Receivable (AR) is all the money your customers owe you for goods or services you’ve already delivered. It’s an asset on your balance sheet because it represents cash that will be flowing into your business soon.

On the flip side, Accounts Payable (AP) is the money you owe to your suppliers. It's a liability on your balance sheet because it’s cash that will be flowing out of your business.

To put it plainly:

- AR is money coming IN.

- AP is money going OUT.

Getting a handle on both sides of this equation is the secret to a healthy, predictable cash flow. When you get paid on time (healthy AR) and manage your own bills smartly (healthy AP), your business is set up for stability and growth.

How Often Should I Reconcile My Accounts Receivable?

For most small and medium-sized businesses in Africa, monthly reconciliation is the gold standard. Treat it like a regular financial check-up. This simple routine helps you catch any little discrepancies—like a payment you forgot to record, a duplicate invoice, or a simple typo—before they spiral into much bigger headaches.

Sticking to a monthly schedule keeps your financial reports accurate, giving you a true picture of where your business stands. That said, if you’re processing a high volume of transactions every day, you might find that a weekly reconciliation gives you even tighter control and helps you spot issues almost immediately.

The whole point of reconciliation is to make sure the numbers in your accounting books perfectly match the numbers on your bank statements. With modern software, this isn't the multi-day slog it used to be. The process can be largely automated, turning a tedious task into a quick, painless review.

When Should I Give Up and Write Off an Invoice as Bad Debt?

Knowing when to call it quits on an unpaid invoice is a tough but crucial decision. There's no magic number that fits every business, but a solid rule of thumb is to start considering an invoice for write-off once it’s 90 to 120 days overdue.

This isn't a step you take lightly. It should only happen after you’ve made every reasonable attempt to collect the payment. Make sure you’ve documented all your efforts, which should include:

- Sending multiple reminder emails at regular intervals.

- Making several follow-up phone calls to your contact.

- Issuing a formal final demand letter that clearly outlines what happens next.

If the client has gone completely silent, gone out of business, or is fighting the charge without a good reason, those are all strong signs the debt is now uncollectible. Your accounts receivable ageing report is your best friend here—it will help you spot these problem accounts long before they ever hit the 120-day mark.

My Industry Has Long Payment Cycles. Can I Still Improve My Cash Flow?

Absolutely. Even if you're stuck in an industry where 60 or 90-day payment terms are the norm, you’re not powerless. There are a few smart strategies you can use to nudge clients to pay faster.

First, try offering a small discount for early payment. A simple term like “2/10, Net 60” gives your client a 2% discount if they pay within 10 days. You’d be surprised how effective a small incentive can be at moving your invoice to the top of their to-do list.

Second, make it ridiculously easy for them to pay you. In the African market, that means going beyond a simple bank transfer. Integrating mobile money platforms like M-PESA or popular payment gateways like Flutterwave and Paystack lets clients settle their bills in just a few clicks.

Finally, you could look into invoice financing. This is where a third-party company gives you a large chunk of the invoice’s value upfront. It gives you immediate cash while they take on the task of collecting the full amount. For businesses struggling to bridge cash flow gaps, this can be a real lifeline.

Ready to turn your accounts receivable from a source of stress into a smooth, reliable cash flow engine? CRM Africa brings it all together on one platform. We automate your invoicing, integrate with M-PESA and other African payment gateways, and provide client-branded portals to help you get paid faster and easier than ever. Schedule a free consultation or Demo to see how you can take control of your finances today.